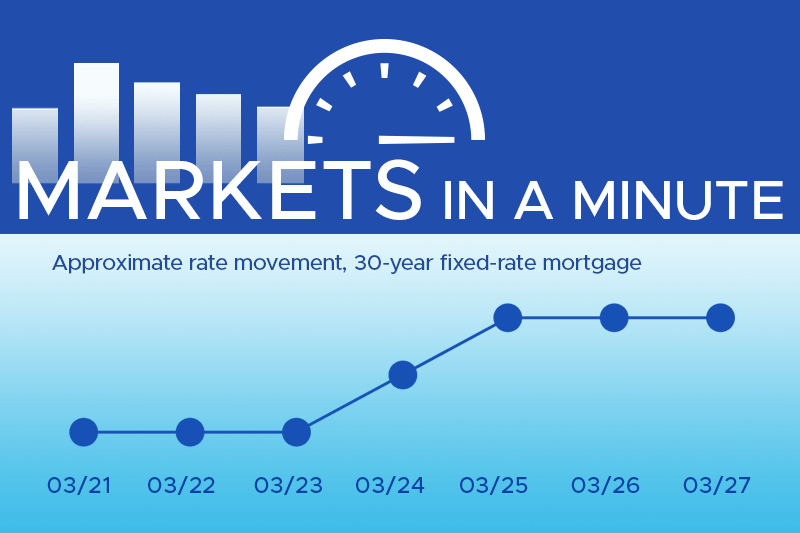

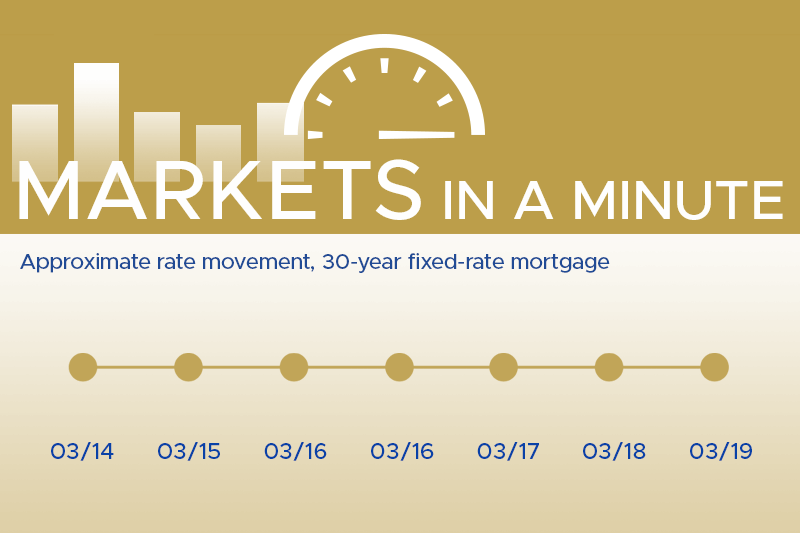

At Thompson Kane, we stay ahead of shifting market trends so you don’t have to.…

A Practical Guide to the Home Mortgage Process at Thompson Kane

If you’re a first-time homebuyer or simply new to the mortgage process, the road ahead may seem complicated. However, understanding the key steps and preparing properly can make your journey toward homeownership much smoother. In this guide, we’ll walk through the basics of what you can expect during the mortgage process, from loan options to closing day and beyond. Check out the links below for articles that expand on each topic.

Understanding Loan Options

Before applying for a mortgage, it’s important to explore the different loan programs available. These include options like Conventional loans, FHA loans, VA loans, and USDA loans. Each loan type has its own set of benefits and eligibility requirements. For example, FHA loans are popular among first-time buyers because they require a lower down payment, while VA loans offer exclusive benefits for veterans and active military members.

Learn more about mortgage options here

Preparing Your Documents for the Mortgage Process

One of the first steps in the mortgage process is gathering the necessary documents. Lenders require documentation to verify your income, employment, assets, and creditworthiness. Here’s a quick rundown of what you’ll need to apply:

- Proof of income (pay stubs, tax returns, W-2s)

- Bank statements (to verify savings and assets)

- Credit report

- Photo ID

- Proof of employment

You’ll need to provide these documents multiple times throughout the mortgage process, but you can avoid last minute scrambling if you get them together early.

Check out our expanded guide on preparing documents here

Key Mortgage Milestones and Timing

The mortgage process typically follows several key stages, each with important milestones. Here’s a general overview of how it all fits together:

- Pre-approval: Before you start house hunting, it’s a good idea to get pre-approved for a mortgage. This involves a preliminary review of your financials and gives you an idea of how much house you can afford. Pre-approval also strengthens your position when making an offer on a home.

- Finding a Realtor: After securing pre-approval, many buyers begin working with a real estate agent. A realtor can help you navigate the housing market, find listings, and ultimately make an offer on a home.

More on why a real estate agent can be a game-changer here - Making an Offer: Once you’ve found a home, your realtor will guide you through making a formal offer. If the offer is accepted, you’ll move into the loan application phase of the mortgage process.

- Loan Application and Underwriting: After your offer is accepted, the official loan process begins. At this point in the mortgage process, you’ll need to submit updated versions of the documents you gathered at pre-approval. Documents such as paystubs or bank statements must be as current as possible. The lender will then enter the underwriting stage, where they thoroughly review your financial background. This process typically takes a few weeks.

- Appraisal and Inspection: During underwriting, the lender will also require an appraisal to ensure the home is worth the loan amount. Additionally, you’ll want to schedule a home inspection to uncover any potential issues with the property. Learn more about home inspections here

- Closing: After underwriting is complete and the appraisal meets the lender’s criteria, it’s time for closing, the final stage of the mortgage process. At this stage, you’ll review and sign all the loan documents, officially becoming the homeowner. Closing is also when you’ll pay your closing costs and down payment.

Learn more about closing costs

What Happens After Closing in the Mortgage Process?

Once you’ve closed on your mortgage and have the keys in hand, you’ll start making your monthly payments. It’s important to budget for additional homeownership expenses such as property taxes, insurance, and any required maintenance or repairs. Learn more about the financial aspects of homeownership

Additionally, it’s common for your mortgage to be sold to another lender after closing. This is a standard practice in the mortgage process, and it doesn’t affect the terms of your loan. You’ll receive a notice in the mail when your loan is transferred, and you’ll be informed where to send your payments. While it might feel unsettling to have your loan passed to another company, rest assured this transfer has no impact on your loan itself—just the servicer who handles your payments.

Moving Forward

Now that you have a basic overview of the mortgage process, you’re better prepared for each step on the road to homeownership. Remember, while this guide provides a starting point, there are many more details to explore. Refer to our blog for deeper insights on important topics like down payments, credit scores, refinancing, and more. Whether you’re just beginning or nearing closing day, our goal is to provide the resources you need to make informed, confident decisions.

If you have any specific questions or are ready to start the conversation about your mortgage, reach out to one of Thompson Kane’s experienced loan officers today!

Related Posts