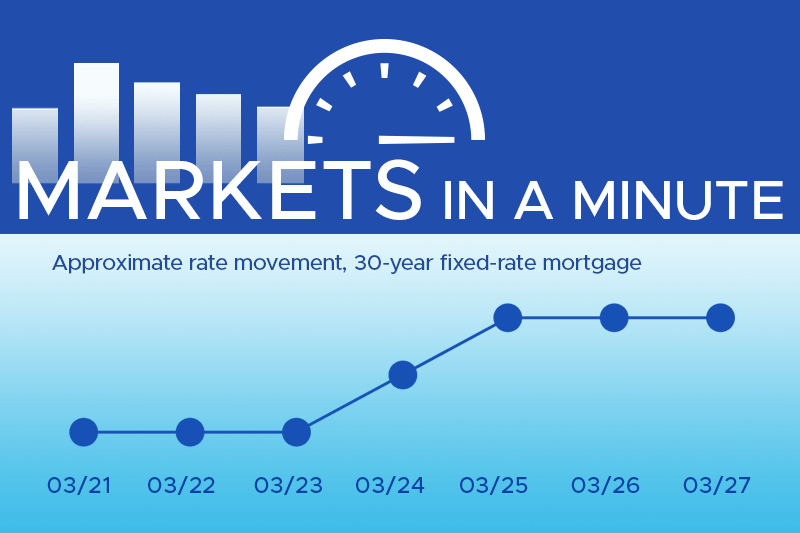

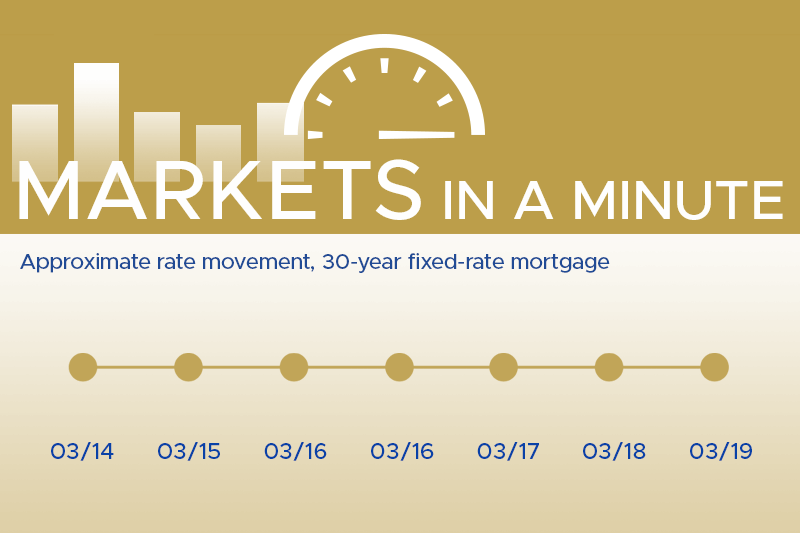

At Thompson Kane, we stay ahead of shifting market trends so you don’t have to.…

Strategies to Get the Lowest Mortgage Interest Rate: 7 Key Tips

Purchasing a home is one of the most significant financial commitments you’ll ever make, and securing the lowest possible mortgage interest rate can save you thousands of dollars over the life of your loan. At Thompson Kane & Company, we understand that every dollar counts, and we’re here to help you navigate the mortgage process. Here are eight key strategies to help you get the lowest mortgage interest rate possible.

1. Improve Your Credit Score

Your credit score is one of the most critical factors lenders consider when determining your mortgage interest rate. Higher credit scores typically qualify for lower

rates. To boost your score:

- Pay all bills on time.

- Reduce outstanding debt.

- Avoid opening new credit accounts right before applying for a mortgage.

- Regularly check your credit report for errors and dispute any inaccuracies.

2. Increase Your Down Payment

The more money you put down upfront, the less risky you appear to lenders. A larger down payment often leads to a lower interest rate. Aim for at least 20% of the home’s purchase price if possible. This not only helps you secure a better rate but also eliminates the need for private mortgage insurance (PMI).

3. Consider a Shorter Loan Term

While 30-year mortgages are common, they usually come with higher interest rates than shorter-term loans. If you can afford higher monthly payments, consider a 15 or 20-year mortgage. These loans typically offer lower rates, and you’ll pay less interest over the life of the loan.

4. Lock in Your Rate

Mortgage rates can fluctuate daily. Once you find a rate you’re comfortable with, ask your lender to lock it in. This rate lock ensures that you’ll get the agreed-upon rate even if interest rates rise before your loan closes. Rate locks can last from 30 to 60 days, or even longer, depending on the lender.

5. Pay for Discount Points

Discount points are upfront fees paid to the lender at closing in exchange for a lower interest rate. One point typically costs 1% of your mortgage amount and can reduce your interest rate by about 0.25%. If you plan to stay in your home for a long time, buying points can be a wise investment that saves you money in the long run.

6. Consider an Adjustable-Rate Mortgage (ARM)

If you don’t plan on staying in your home for more than a few years, an ARM might be a good option. ARMs offer lower initial interest rates than fixed-rate mortgages. However, be aware that the rate will adjust periodically after the initial fixed-rate period, which could lead to higher payments in the future.

7. Strengthen Your Financial Profile

Summing it Up

Securing the lowest mortgage interest rate requires careful planning and strategy. By improving your credit score, increasing your down payment, considering shorter loan terms, locking in your rate, paying for discount points, exploring adjustable-rate mortgages, and strengthening your financial profile, you can significantly reduce the cost of your mortgage over time.

At Thompson Kane & Company, our team of lending experts is ready to help you navigate the mortgage process and find the best rate for your unique situation. Contact us today to discuss your options and develop a personalized strategy to secure your dream home with the best possible terms. We’re here to ensure you make the most of your mortgage and achieve your homeownership goals.

Related Posts