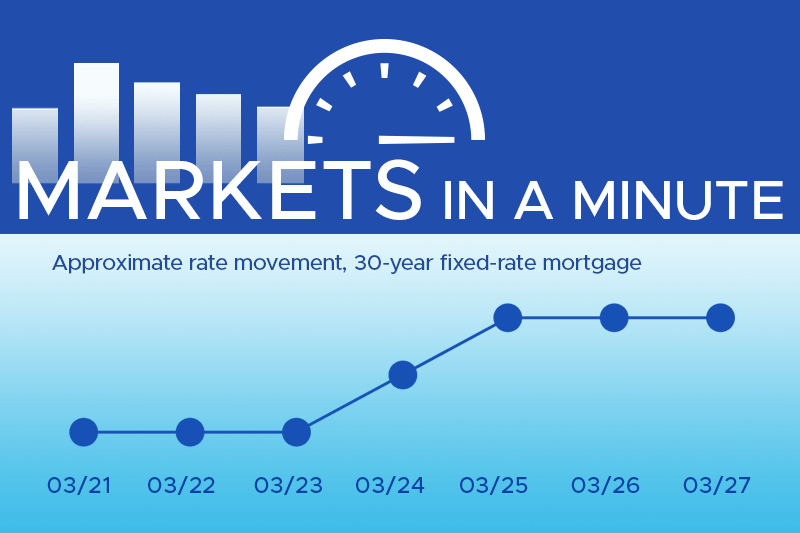

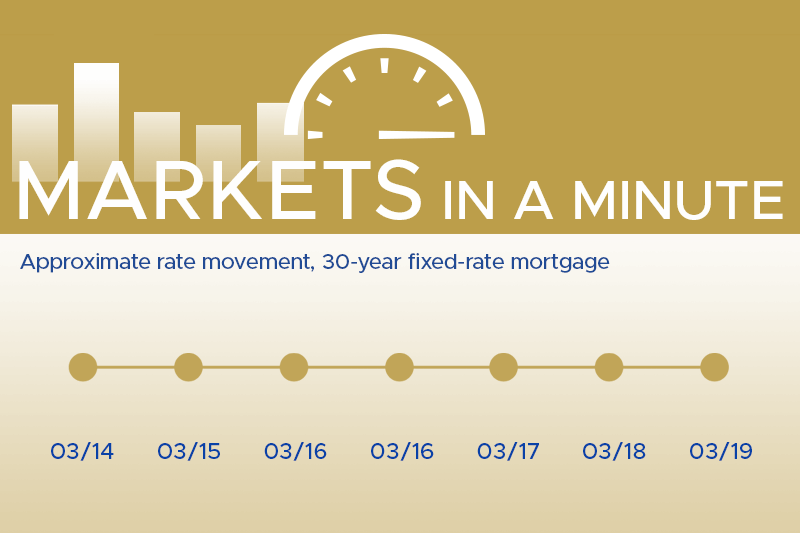

At Thompson Kane, we stay ahead of shifting market trends so you don’t have to.…

Homeowner’s Insurance and PMI: What Homebuyers Need to Know

As a homeowner or prospective buyer, understanding homeowner’s insurance and Private Mortgage Insurance (PMI) is crucial. This guide will help you navigate these important aspects of home ownership.

Homeowner’s Insurance Basics

Homeowner’s insurance protects your property and belongings from damage or loss. While not legally mandated, mortgage lenders typically require it. The most common policy offers broad coverage for the structure and named perils for personal property.

Here are 4 key things you should know about home owner’s insurance:

- Coverage limits should be sufficient to rebuild your home and replace belongings.

- Understand the difference between Actual Cash Value and Replacement Cost coverage.

- Know your policy’s exclusions and consider additional coverage if needed.

- Liability coverage protects you if someone is injured on your property.

Saving on Homeowner’s Insurance:

- Shop around and compare quotes.

- Consider a higher deductible for lower premiums.

- Bundle policies (e.g., home and auto) for discounts.

- Improve home security with smoke detectors and alarm systems.

- Maintain good credit, as many insurers use credit scores to determine premiums.

- Ask about discounts for loyalty, retirees, or recent home improvements.

Additional Coverage Options:

While standard policies cover many risks, you might need additional coverage for specific situations. Flood insurance, earthquake coverage, or protection for high-value items are examples. Consult your insurance agent to determine if these are necessary for your situation.

Understanding Private Mortgage Insurance (PMI)

PMI is a type of insurance that protects the lender, not the homeowner. It’s typically required when you put down less than 20% on a conventional mortgage.

4 key things to know about PMI:

- Purpose: PMI protects the lender if you default on your loan.

- Cost: Usually 0.5% to 1% of the loan amount annually, added to your monthly mortgage payment.

- Duration: Required until you reach 20% equity in your home.

- Removal: By law, if the homeowner is current on mortgage payments and meeting lender requirements, PMI must be terminated when you reach 22% equity based on the original value. You can request removal at 20% equity.

How PMI Differs from Homeowner’s Insurance:

- PMI protects the lender; homeowner’s insurance protects you.

- PMI doesn’t cover property damage or liability.

- Homeowner’s insurance is always required by lenders; PMI is only required with less than 20% down.

Avoiding or Removing PMI:

- Make a 20% down payment.

- Consider a piggyback loan (80-10-10 loan) to avoid PMI.

- Pay down your mortgage aggressively to reach 20% equity faster.

- Refinance once you’ve built sufficient equity.

Advice for First-Time Homebuyers:

- Factor PMI, property taxes, and insurance into your budget when house hunting.

- Save for a larger down payment to avoid PMI if possible.

- Understand that property taxes and insurance are often included in your monthly mortgage payment through an escrow account.

- Get quotes for homeowner’s insurance early in the buying process.

- Consider the long-term insurance implications of different properties (e.g., flood zones, older homes).

Ask Your Lender or Realtor…

- How will PMI impact my monthly mortgage payments?

- How might a specific home’s location, age, and construction affect insurance rates?

- How can I accurately calculate my mortgage, taxes, insurance, PMI, and other home-related costs for my overall budget? Is the home I’m considering within my financial reach?

At Thompson Kane & Company, we’re dedicated to supporting you throughout your home-buying journey. Our experienced loan officers provide the guidance you need to navigate the process successfully. We can assist you in finding an insurance agent and a Realtor who align with your specific goals. Our team is equipped to help you:

- Understand the intricacies of homeowner’s insurance and PMI

- Calculate accurate cost estimates for your potential new home

- Explore options to minimize or avoid PMI

- Find competitive insurance rates

- Connect with trusted professionals in the real estate and insurance industries

We strive to equip you with the financial tools and knowledge needed for a successful home-buying experience. Contact Thompson Kane today to learn how we can help you navigate the current market. We want to help you find and fund your perfect home while making informed financial decisions every step of the way.

Related Posts